In a surprise appearance at the 2026 World Economic Forum in Davos, Elon Musk sat down with BlackRock CEO Larry Fink to discuss the engineering challenges of the coming decade. The conversation laid out an aggressive timeline for AI, robotics, and the colonization of space, framed by Musk’s goal of maximizing the future of human consciousness.

⚡ TL;DR

Elon Musk predicts AI will surpass individual human intelligence by the end of 2026 and collective human intelligence by 2030. To overcome Earth’s energy bottlenecks, he plans to move AI data centers into space within the next three years, utilizing orbital solar power and the cold vacuum for cooling. Additionally, Tesla’s humanoid robots are slated for public sale by late 2027.

🚀 Key Takeaways

The Intelligence Explosion: AI is expected to be smarter than any single human by the end of 2026, and smarter than all of humanity combined by 2030 or 2031.

Orbital Compute: SpaceX aims to launch solar-powered AI data centers into space within 2–3 years to leverage 5x higher solar efficiency and natural cooling.

Robotics for the Public: Humanoid “Optimus” robots are currently in factory testing; public availability is targeted for the end of 2027.

Starship Reusability: SpaceX expects to prove full rocket reusability this year, which would decrease the cost of space access by 100x.

Solving Aging: Musk views aging as a “synchronizing clock” across cells that is likely a solvable problem, though he cautions against societal stagnation if people live too long.

📝 Detailed Summary

The discussion opened with a look at the massive compounded returns of Tesla and BlackRock, establishing the scale at which both leaders operate. Musk emphasized that his ventures—SpaceX, Tesla, and xAI—are focused on expanding the “light of consciousness” and ensuring civilization can survive major disasters by becoming multi-planetary.

Musk identified electrical power as the primary bottleneck for AI. He noted that chip production is currently outpacing the grid’s ability to support them. His “no-brainer” solution is space-based AI. By moving data centers to orbit, companies can bypass terrestrial power constraints and weather cycles. He also highlighted China’s massive lead in solar deployment compared to the U.S., where high tariffs have slowed the transition.

The conversation concluded with Musk’s “philosophy of curiosity.” He shared that his drive stems from wanting to understand the meaning of life and the nature of the universe. He remains an optimist, arguing that it is better to be an optimist and wrong than a pessimist and right.

🧠 Thoughts

The most striking part of this talk is the shift toward space as a practical infrastructure solution for AI, rather than just a destination for exploration. If SpaceX achieves full reusability this year, the economic barrier to launching heavy data centers disappears. We are moving from the era of “Internet in the cloud” to “Intelligence in the stars.” Musk’s timeline for AGI (Artificial General Intelligence) also feels increasingly urgent, putting immense pressure on global regulators to keep pace with engineering.

In a landmark interview on the Moonshots with Peter Diamandis podcast (January 2026), legendary futurist Ray Kurzweil discusses the accelerating path to the Singularity. He reaffirms his prediction of Artificial General Intelligence (AGI) by 2029 and the Singularity by 2045, where humans will merge with AI to become 1,000x smarter. Key discussions include reaching Longevity Escape Velocity by 2032, the emergence of “Computronium,” and the transition to a world where biological and digital intelligence are indistinguishable.

Key Takeaways

Predictive Accuracy: Kurzweil maintains an 86% accuracy rate over 30 years, including his 1989 prediction for AGI in 2029.

The Singularity Definition: Defined as the point where we multiply our intelligence 1,000-fold by merging our biological brains with computational intelligence.

Longevity Escape Velocity (LEV): Predicted to occur by 2032. At this point, science will add more than one year to your remaining life expectancy for every year that passes.

The End of “Meat” Limitations: While biological bodies won’t necessarily disappear, they will be augmented by nanotechnology and 3D-printed/replaced organs within a decade or two.

Economic Liberation: Universal Basic Income (UBI) or its equivalent will be necessary by the 2030s as the link between labor and financial survival is severed.

Computronium: By 2045, we will be able to convert matter into “computronium,” the optimal form of matter for computation.

Detailed Summary

The Road to 2029 and 2045

Ray Kurzweil emphasizes that the current pace of change is so rapid that a “one-year prediction” is now considered long-term. He stands firm on his timeline: AGI will be achieved by 2029. He distinguishes AGI from the Singularity (2045), explaining that while AGI represents human-level proficiency across all fields, the Singularity is the total merger with that intelligence. By then, we won’t be able to distinguish whether an idea originated from our biological neurons or our digital extensions.

Longevity and Health Reversal

One of the most exciting segments of the discussion centers on health. Kurzweil predicts we are only years away from being able to simulate human biology perfectly. This will allow for “billions of tests in a weekend,” leading to cures for cancer and heart disease. He personally utilizes advanced therapies to maintain “zero plaque” in his arteries, advising everyone to “stay healthy enough” to reach the early 2030s, when LEV becomes a reality.

Digital Immortality and Avatars

The conversation touches on “Plan D”—Cryonics—but Kurzweil prefers “Plan A”: staying alive. However, he is already working on digital twins. He mentions that by the end of 2026, he will have a functional AI avatar based on his 11 books and hundreds of articles. This avatar will eventually be able to conduct interviews and remember his life better than he can himself.

The Future of Work and Society

As AI handles the bulk of production, the concept of a “job” will shift from a survival necessity to a search for gratification. Kurzweil believes this will be a liberating transition for the 79% of employees who currently find no meaning in their work. He remains a “10 out of 10” on the optimism scale regarding humanity’s future.

Analysis & Thoughts

What makes this 2026 update so profound is that Kurzweil isn’t moving his goalposts. Despite the massive AI explosion of the mid-2020s, his 1989 predictions remain on track. The most striking takeaway is the shift from AI being an “external tool” to an “internal upgrade.” The ethical debates of today regarding “AI personhood” may soon become moot because we will be the AI.

The concept of Computronium and disassembling matter to fuel intelligence suggests a future that is almost unrecognizable by today’s standards. If Kurzweil is even half right about 2032’s Longevity Escape Velocity, the current generation may be the last to face “natural” death as an inevitability.

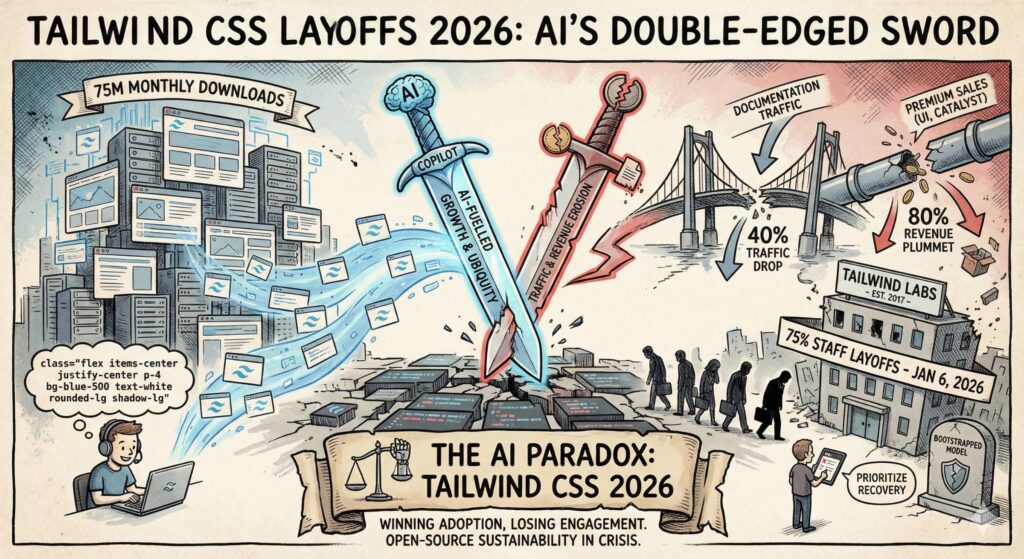

TL;DR (January 9, 2026 Update): Generative AI has delivered a double blow to core developer resources. Tailwind CSS, despite exploding to 75M+ monthly downloads, suffered an ~80% revenue drop as AI tools generate utility-class code instantly—bypassing docs and premium product funnels—leading Tailwind Labs to lay off 75% of its engineering team (3 out of 4 engineers) on January 7. Within 48 hours, major sponsors including Google AI Studio, Vercel, Supabase, Gumroad, Lovable, and others rushed in to support the project. Meanwhile, Stack Overflow’s public question volume has collapsed (down ~77–78% from 2022 peaks, back to 2009 levels), yet revenue doubled to ~$115M via AI data licensing deals and enterprise tools like Stack Internal (used by 25K+ companies). This is the live, real-time manifestation of AI “strip-mining” high-quality knowledge: it supercharges adoption while starving the sources. Developers must urgently adapt—embrace AI as an amplifier, pivot to irreplaceable human skills, and build proprietary value—or face obsolescence.

Key Takeaways: The Harsh, Real-Time Lessons from January 2026

AI boosts usage dramatically (Tailwind’s 75M+ downloads/month) but destroys traffic-dependent revenue models by generating perfect code without needing docs or forums.

Small teams are especially vulnerable: Tailwind Labs reduced from 4 to 1 engineer overnight due to an 80% revenue crash—yet the framework itself thrives thanks to AI defaults.

Community & Big Tech respond fast: In under 48 hours after the layoffs announcement, sponsors poured in (Google AI Studio, Vercel, Supabase, etc.), turning a crisis into a “feel-good” internet moment.

Stack Overflow’s ironic success: Public engagement cratered (questions back to 2009 levels), but revenue doubled via licensing its 59M+ posts to AI labs and launching enterprise GenAI tools.

Knowledge homogenization accelerates: AI outputs default to Tailwind patterns, creating uniform “AI-look” designs and reducing demand for original sources.

The “training data cliff” risk is real: If human contributions dry up (fewer new SO questions, less doc traffic), AI quality on fresh/edge-case topics will stagnate.

Developer sentiment is mixed: 84% use or plan to use AI tools, but trust in outputs has dropped to ~29%, with frustration over “almost-right” suggestions rising.

Open-source business models must evolve: Shift from traffic/ads/premium upsells to direct sponsorships, data licensing, enterprise features, or AI-integrated services.

Human moats endure: Complex architecture, ethical judgment, cross-team collaboration, business alignment, and change management remain hard for AI to replicate fully.

Adaptation is survival: Top developers now act as AI orchestrators, system thinkers, and value creators rather than routine coders.

Detailed Summary: The Full January 2026 Timeline & Impact

As of January 9, 2026, the developer world is reeling from a perfect storm of AI disruption hitting two iconic projects simultaneously.

Tailwind CSS Crisis & Community Response (January 7–9, 2026)

Adam Wathan, creator of Tailwind CSS, announced on January 7 that Tailwind Labs had to lay off 75% of its engineering team (3 out of 4 engineers). In a raw, emotional video walk and GitHub comments, he blamed the “brutal impact” of AI: the framework’s atomic utility classes are perfect for LLM code generation, leading to massive adoption (75M+ monthly downloads) but a ~40% drop in documentation traffic since 2023 and an ~80% revenue plunge. Revenue came from premium products like Tailwind UI and Catalyst—docs served as the discovery funnel, now short-circuited by tools like Copilot, Cursor, Claude, and Gemini.

The announcement sparked an outpouring of support. Within 24–48 hours, major players announced sponsorships: Google AI Studio (via Logan Kilpatrick), Vercel, Supabase, Gumroad, Lovable, Macroscope, and more. Adam clarified that Tailwind still has “a fine business” (just not great anymore), with the partner program now funding the open-source core more directly. He remains optimistic about experimenting with new ideas in a leaner setup.

Stack Overflow’s Parallel Pivot

Stack Overflow’s decline started earlier (post-ChatGPT in late 2022) but accelerated: monthly questions fell ~77–78% from 2022 peaks, returning to 2009 levels (3K–7K/month). Yet revenue roughly doubled to $115M (FY 2025–2026), with losses cut dramatically. The secret? Licensing its massive, human-curated Q&A archive to AI companies (OpenAI, Google, etc.)—similar to Reddit’s $200M+ deals—and launching enterprise products like Stack Internal (GenAI powered by SO data, used by 25K+ companies) and AI Assist.

This creates a vicious irony: AI trained on SO and Tailwind data, commoditizes it, reduces human input, and risks a “training data cliff” where models stagnate on new topics. Meanwhile, homogenized outputs fuel demand for unique, human-crafted alternatives.

Future-Proofing Your Developer Career: In-Depth 2026 Strategies

AI won’t erase developer jobs (projections still show ~17% growth through 2033), but it will automate routine coding. Winners will leverage AI while owning what machines can’t replicate. Here’s a detailed, actionable roadmap:

Master AI Collaboration & Prompt Engineering: Pick one powerhouse tool (Cursor, Claude, Copilot, Gemini) and become fluent. Use advanced prompting for complex tasks; always validate for security, edge cases, performance, and hallucinations. Chain agents (e.g., via LangChain) for multi-step workflows. Integrate daily—let AI handle boilerplate while you focus on oversight.

Elevate to Systems Architecture & Strategic Thinking: AI excels at syntax; humans win on trade-offs (scalability vs. cost vs. maintainability), business alignment (ROI, user impact), and risk assessment. Study domain-driven design, clean architecture, and system design interviews. Become the “AI product manager” who defines what to build and why.

Build Interdisciplinary & Human-Centric Skills: Hone communication (explaining trade-offs to stakeholders), leadership, negotiation, and domain knowledge (fintech, healthcare, etc.). Develop soft skills like change management and ethics—areas where AI still struggles. These create true moats.

Create Proprietary & Defensible Assets: Own your data, custom fine-tunes, guardrailed agents, and unique workflows. For freelancers/consultants: specialize in AI integration, governance, risk/compliance, or hybrid human-AI systems. Document patterns that AI can’t easily replicate.

Commit to Lifelong, Continuous Learning: Follow trends via newsletters (Benedict Evans), podcasts (Lex Fridman), and communities. Pursue AI/ML certs, experiment with emerging agents, and audit your workflow quarterly: What can AI do better? What must remain human?

Target Resilient Roles & Mindsets: Seek companies heavy on AI innovation or physical-world domains. Aim for roles like AI Architect, Prompt Engineer, Agent Orchestrator, or Knowledge Curator. Mindset shift: Compete by multiplying AI, not against it.

Start small: Build a side project with AI agents, then manually optimize it. Network in Toronto’s scene (MaRS, meetups). Experiment relentlessly—the fastest adapters will define the future.

Navigating the AI Era in 2026 and Beyond

January 2026 feels like a knowledge revolution turning point—AI democratizes access but disrupts gatekeepers. The “training data cliff” is a genuine risk: without fresh human input, models lose edge on novelty. Yet the response to Tailwind’s crisis shows hope—community and Big Tech stepping up to sustain the ecosystem.

Ethically, attribution matters: AI owes a debt to SO contributors and Tailwind’s patterns—better licensing, revenue shares, or direct funding could help. For developers in Toronto’s vibrant hub, opportunities abound in AI consulting, hybrid tools, and governance.

This isn’t the death of development—it’s evolution into a more strategic, amplified era. View AI as an ally, stay curious, keep building, and remember: human ingenuity, judgment, and connection will endure.

TLDR: Tailwind Labs, creators of the popular Tailwind CSS framework, laid off 75% of its engineering team on January 6, 2026, due to AI-driven disruptions. While AI boosted Tailwind’s popularity with 75 million monthly downloads, it slashed documentation traffic by 40% and revenue by 80%, as developers rely on AI tools like GitHub Copilot instead of visiting the site. This “AI paradox” highlights vulnerabilities in open-source business models, sparking community debates on sustainability and future adaptations.

Key Takeaways

Tailwind CSS’s explosive growth is fueled by AI coding agents generating its code by default, leading to ubiquity in modern web development but bypassing traditional learning and monetization channels.

Documentation site traffic dropped 40% since early 2023, crippling upsells for premium products like Tailwind UI and Catalyst, as AI handles queries without site visits.

Revenue plummeted 80%, forcing drastic layoffs in the bootstrapped company, with no venture backing to cushion the blow.

The announcement came via a GitHub PR comment, going viral on X, Hacker News, and Reddit, eliciting sympathy, irony, and calls for pivots or acquisitions.

Broader implications include risks for other doc-heavy tools, reduced deep learning among developers, and acceleration of open-source commoditization by AI.

Potential futures: Short-term focus on maintenance, long-term shifts to AI-integrated products, partnerships, or new revenue streams like subscriptions.

Detailed Summary

Tailwind CSS, launched in 2017 by Adam Wathan and Steve Schoger, revolutionized web development with its utility-first approach. Developers apply classes directly in HTML for rapid UI building, integrating seamlessly with frameworks like React and Next.js. Tailwind Labs monetizes through premium offerings while keeping the core framework open-source and free.

The crisis unfolded on January 6, 2026, when Wathan announced in a GitHub pull request that 75% of the engineering team was laid off. The PR proposed an “AGENTS.md” file for guiding LLMs to generate Tailwind code optimally. Wathan rejected it, citing the need to prioritize business recovery over community features.

In his comment, Wathan explained: Traffic to tailwindcss.com fell 40% despite rising popularity, as AI tools like Copilot and Claude output Tailwind code without users needing docs. This site was crucial for promoting paid products, leading to an 80% revenue drop. Contributor Michael Sears warned of potential “abandonware” without sustainable funding.

The news exploded online. On X (formerly Twitter), posts like one from @ybhrdwj amassed thousands of likes, highlighting the irony. Discussions on Hacker News (over 465 comments) and Reddit’s r/theprimeagen debated AI’s commoditization of knowledge. Media outlets like DevClass and OfficeChai framed it as a warning for traffic-reliant businesses.

Community reactions mixed shock with suggestions: Pivot like avoiding Kodak’s fate, shame Big Tech for non-contribution, or pursue acquisitions by firms like Vercel or Anthropic.

Some Thoughts on the AI Paradox and Open-Source Future

This situation exemplifies AI’s disruptive power—boosting adoption while eroding foundations. Tailwind “won” by becoming AI’s default CSS choice but lost human engagement essential for monetization. It’s a wake-up call for bootstrapped startups: Relying on organic traffic is precarious when AI answers queries instantly.

For developers, AI enhances productivity but risks shallower skills, potentially flooding codebases with unvetted “junk.” Hiring may favor those who can curate AI outputs effectively.

Open-source sustainability feels more fragile; premium add-ons falter as AI replicates value for free. Alternatives like enterprise support or AI partnerships could emerge. Tailwind’s resilience lies in its community—if it adapts to AI-native tools, it could thrive. Otherwise, it risks fading, underscoring that in 2026, AI reshapes value chains relentlessly.

TL;DR: Google is supercharging Gmail with Gemini AI, introducing features like AI Overviews for instant answers from your inbox, Help Me Write for drafting emails, Suggested Replies, Proofread, and an upcoming AI Inbox for prioritizing tasks. Many roll out today for free, with premium options for subscribers, starting in the US and expanding globally.

Key Takeaways

AI Overviews: Summarizes long email threads and answers natural language questions like “Who quoted my bathroom renovation?” – free conversation summaries today, full Q&A for Google AI Pro/Ultra subscribers.

Help Me Write & Suggested Replies: Draft or polish emails from scratch, with context-aware one-click responses in your style – available to everyone for free starting today.

Proofread: Advanced checks for grammar, tone, and style – exclusive to Google AI Pro/Ultra subscribers.

AI Inbox: A personalized briefing that highlights to-dos, prioritizes VIPs, and filters clutter securely – coming soon for trusted testers, broader rollout in months.

Personalization Boost: Next month, Help Me Write integrates context from other Google apps for better tailoring.

Availability: Powered by Gemini 3, starting in US English today, with more languages and regions soon. Link to original announcement: Google Blog Post.

Detailed Summary

Google’s latest announcement marks a pivotal shift for Gmail, transforming it from a simple email client into an intelligent, proactive assistant powered by Gemini AI. With over 3 billion users worldwide, Gmail has evolved since its 2004 launch, but rising email volumes have made inbox management a daily battle. Enter the “Gemini era,” where AI takes center stage to streamline your workflow.

At the heart of these updates is AI Overviews, inspired by Google Search’s AI summaries. This feature eliminates the need for manual digging through emails. For lengthy threads, it provides a concise breakdown of key points right when you open the message. Even better, you can query your entire inbox in natural language—think asking for specific details from old quotes or reservations—and Gemini’s reasoning engine delivers an instant overview with the exact info you need. Conversation summaries are free for all users starting today, while the full question-answering capability is reserved for paid Google AI Pro and Ultra plans.

Productivity gets a major upgrade with Help Me Write, now available to everyone, allowing you to draft emails from scratch or refine existing ones. Paired with Suggested Replies (an evolution of Smart Replies), it analyzes conversation context to suggest responses that mimic your personal writing style—perfect for quick coordination like family events. Just tap to use or tweak. For that extra polish, Proofread offers in-depth reviews of grammar, tone, and style, ensuring your emails are professional and on-point. Help Me Write and Suggested Replies are free, but Proofread requires a subscription.

Looking ahead, the AI Inbox promises to redefine how you start your day. It acts as a smart filter, surfacing critical updates like bill deadlines or appointment reminders while burying the noise. By analyzing signals such as frequent contacts and message content (all done privately on Google’s secure systems), it identifies VIPs and to-dos, giving you a personalized snapshot. Trusted testers get early access, with a full launch in the coming months.

These features are fueled by the advanced Gemini 3 model, ensuring speed and accuracy. Rollouts begin today in the US for English users, with expansions to more languages and regions planned. Next month, Help Me Write will pull in data from other Google apps for even smarter personalization.

Some Thoughts

This Gemini integration could be a game-changer for overwhelmed inboxes, turning Gmail into a true AI sidekick that anticipates needs rather than just storing messages. It’s exciting to see free access for core features, democratizing AI for everyday users, but the premium gating on advanced tools like full AI Overviews and Proofread might frustrate non-subscribers. Privacy remains a hot topic—Google emphasizes secure processing, but users should stay vigilant about data controls. Overall, in a world drowning in emails, this feels like a timely evolution that could boost productivity without sacrificing usability. If it delivers on the hype, competitors like Outlook might need to play catch-up fast.

In a wide-ranging discussion on the No Priors Podcast, NVIDIA Founder and CEO Jensen Huang reflects on the rapid evolution of artificial intelligence throughout 2025 and provides a strategic roadmap for 2026. From the debunking of the “AI Bubble” to the rise of physical robotics and the “ChatGPT moments” coming for digital biology, Huang offers a masterclass in how accelerated computing is reshaping the global economy.

TL;DW (Too Long; Didn’t Watch)

The Core Shift: General-purpose computing (CPUs) has hit a wall; the world is moving permanently to accelerated computing.

The Jobs Narrative: AI automates tasks, not purposes. It is solving labor shortages in manufacturing and nursing rather than causing mass unemployment.

The 2026 Breakthrough: Digital biology and physical robotics are slated for their “ChatGPT moment” this year.

Geopolitics: A nuanced, constructive relationship with China is essential, and open source is the “innovation flywheel” that keeps the U.S. competitive.

Key Takeaways

Scaling Laws & Reasoning: 2025 proved that scaling compute still translates directly to intelligence, specifically through massive improvements in reasoning, grounding, and the elimination of hallucinations.

The End of “God AI”: Huang dismisses the myth of a monolithic “God AI.” Instead, the future is a diverse ecosystem of specialized models for biology, physics, coding, and more.

Energy as Infrastructure: AI data centers are “AI Factories.” Without a massive expansion in energy (including natural gas and nuclear), the next industrial revolution cannot happen.

Tokenomics: The cost of AI inference dropped 100x in 2024 and could drop a billion times over the next decade, making intelligence a near-free commodity.

DeepSeek’s Impact: Open-source contributions from China, like DeepSeek, are significantly benefiting American startups and researchers, proving the value of a global open-source ecosystem.

Detailed Summary

The “Five-Layer Cake” of AI

Huang explains AI not as a single app, but as a technology stack: Energy → Chips → Infrastructure → Models → Applications. He emphasizes that while the public focuses on chatbots, the real revolution is happening in “non-English” languages, such as the languages of proteins, chemicals, and physical movement.

Task vs. Purpose: The Future of Labor

Addressing the fear of job loss, Huang uses the “Radiologist Paradox.” While AI now powers nearly 100% of radiology applications, the number of radiologists has actually increased. Why? Because AI handles the task (scanning images), allowing the human to focus on the purpose (diagnosis and research). This same framework applies to software engineers: their purpose is solving problems, not just writing syntax.

Robotics and Physical AI

Huang is incredibly optimistic about robotics. He predicts a future where “everything that moves will be robotic.” By applying reasoning models to physical machines, we are moving from “digital rails” (pre-programmed paths) to autonomous agents that can navigate unknown environments. He foresees a trillion-dollar repair and maintenance industry emerging to support the billions of robots that will eventually inhabit our world.

The “Bubble” Debate

Is there an AI bubble? Huang argues “No.” He points to the desperate, unsatisfied demand for compute capacity across every industry. He notes that if chatbots disappeared tomorrow, NVIDIA would still thrive because the fundamental architecture of the world’s $100 trillion GDP is shifting from CPUs to GPUs to stay productive.

Analysis & Thoughts

Jensen Huang’s perspective is distinct because he views AI through the lens of industrial production. By calling data centers “factories” and tokens “output,” he strips away the “magic” of AI and reveals it as a standard industrial revolution—one that requires power, raw materials (data/chips), and specialized labor.

His defense of Open Source is perhaps the most critical takeaway for policymakers. By arguing that open source prevents “suffocation” for startups and 100-year-old industrial companies, he positions transparency as a national security asset rather than a liability. As we head into 2026, the focus is clearly shifting from “Can the model talk?” to “Can the model build a protein or drive a truck?”

In a wide-ranging, three-hour deep dive recorded at the Tesla Gigafactory, Elon Musk sat down with Peter Diamandis and Dave Blundin to map out a future that feels more like science fiction than reality. From the “supersonic tsunami” of AI to the launch of orbital data centers, Musk’s 2026 vision is a blueprint for a world defined by radical abundance, universal high income, and the dawn of the technological singularity.

⚡ TLDW (Too Long; Didn’t Watch)

We are currently living through the Singularity. Musk predicts AGI will arrive by 2026, with AI exceeding total human intelligence by 2030. Key bottlenecks have shifted from “code” to “kilowatts,” leading to a massive push for Space-Based Data Centers and solar-powered AI satellites. While the transition will be “bumpy” (social unrest and job displacement), the destination is Universal High Income, where goods and services are so cheap they are effectively free.

🚀 Key Takeaways

The 2026 AGI Milestone: Musk remains confident that Artificial General Intelligence will be achieved by next year. By 2030, AI compute will likely surpass the collective intelligence of all humans.

The “Chip Wall” & Power: The limiting factor for AI is no longer just chips; it’s electricity and cooling. Musk is building Colossus 2 in Memphis, aiming for 1.5 gigawatts of power by mid-2026.

Orbital Data Centers: With Starship lowering launch costs to sub-$100/kg, the most efficient way to run AI will be in space—using 24/7 unshielded solar power and the natural vacuum for cooling.

Optimus Surgeons: Musk predicts that within 3 to 5 years, Tesla Optimus robots will be more capable surgeons than any human, offering precise, shared-knowledge medical care globally.

Universal High Income (UHI): Unlike UBI, which relies on taxation, UHI is driven by the collapse of production costs. When labor and intelligence cost near-zero, the price of “stuff” drops to the cost of raw materials.

Space Exploration: NASA Administrator Jared Isaacman is expected to pivot the agency toward a permanent, crude-based Moon base rather than “flags and footprints” missions.

📝 Detailed Summary

The Singularity is Here

Musk argues that we are no longer approaching the Singularity—we are in it. He describes AI and robotics as a “supersonic tsunami” that is accelerating at a 10x rate per year. The “bootloader” theory was a major theme: the idea that humans are merely a biological bridge designed to give rise to digital super-intelligence.

Energy: The New Currency

The conversation pivoted heavily toward energy as the fundamental “inner loop” of civilization. Musk envisions Dyson Swarms (eventually) and near-term solar-powered AI satellites. He noted that China is currently “running circles” around the US in solar production and battery deployment, a gap he intends to close via Tesla’s Megapack and Solar Roof technologies.

Education & The Workforce

The traditional “social contract” of school-college-job is broken. Musk believes college is now primarily for “social experience” rather than utility. In the future, every child will have an individualized AI tutor (Grock) that is infinitely patient and tailored to their “meat computer” (the brain). Career-wise, the focus will shift from “getting a job” to being an entrepreneur who solves problems using AI tools.

Health & Longevity

While Musk and Diamandis have famously disagreed on longevity, Musk admitted that solving the “programming” of aging seems obvious in retrospect. He emphasized that the goal is not just living longer, but “not having things hurt,” citing the eradication of back pain and arthritis as immediate wins for AI-driven medicine.

🧠 Final Thoughts: Star Trek or Terminator?

Musk’s vision is one of “Fatalistic Optimism.” He acknowledges that the next 3 to 7 years will be incredibly “bumpy” as companies that don’t use AI are “demolished” by those that do. However, his core philosophy is to be a participant rather than a spectator. By programming AI with Truth, Curiosity, and Beauty, he believes we can steer the tsunami toward a Star Trek future of infinite discovery rather than a Terminator-style collapse.

Whether you find it exhilarating or terrifying, one thing is certain: 2026 is the year the “future” officially arrives.

The Ralph Wiggum Loop is a clever technique in AI-assisted programming that creates persistent, iterative loops for coding agents like Anthropic’s Claude Code. Named after the persistent Simpsons character, it allows AIs to keep refining code through repeated attempts until a task is complete, revolutionizing autonomous software development.

Key Takeaways

The Ralph Wiggum Loop emerged in late 2025 and gained popularity in early 2026 as a method for long-running AI coding sessions.

It was originated by developer Geoffrey Huntley, who described it as a simple Bash loop that repeatedly feeds the same prompt to an AI agent.

The technique draws its name from Ralph Wiggum from The Simpsons, symbolizing persistence through mistakes and self-correction.

Core mechanism: An external script or built-in plugin re-injects the original prompt when the AI tries to exit, forcing continued iteration.

Official implementations include Anthropic’s Claude Code plugin called “ralph-wiggum” or commands like “/ralph-loop,” with safeguards like max-iterations and completion strings.

Famous examples include Huntley’s multi-month loop that autonomously built “Cursed,” an esoteric programming language with Gen Z slang keywords.

Users report benefits like shipping multiple repositories overnight or handling complex refactors and tests via persistent AI workflows.

It’s not a traditional loop like for/while in code but a meta-technique for agentic AI, emphasizing persistence over single-pass perfection.

Detailed Summary

The Ralph Wiggum Loop is a groundbreaking technique in AI-assisted programming, popularized in late 2025 and early 2026. It enables autonomous, long-running iterative loops with coding agents like Anthropic’s Claude Code. Unlike one-shot AI interactions where the agent stops after a single attempt, this method keeps the AI working by repeatedly re-injecting the prompt, allowing it to see previous changes (via git history or file state), attempt completions, and loop until success or a set limit is reached.

Developer Geoffrey Huntley originated the concept, simply describing it as “Ralph is a Bash loop”—a basic ‘while true’ script that feeds the same prompt to an AI agent over and over. The AI iterates through errors, self-corrects, and improves across cycles. The name is inspired by Ralph Wiggum from The Simpsons: a lovable, often confused character who persists despite mistakes and setbacks. It embodies the idea of “keep trying forever, even if you’re not getting it right immediately.”

How it works: Instead of letting the AI exit after one pass, the loop intercepts the exit and restarts with the original prompt. The original implementation was an external Bash script for looping AI calls. Anthropic later released an official Claude Code plugin called “ralph-wiggum” (or commands like “/ralph-loop”). This uses a “Stop hook” to handle exits internally—no external scripting needed. Safeguards include options like “–max-iterations” to prevent infinite loops, completion promises (e.g., outputting a string like “COMPLETE” to stop), and handling for stuck states.

Famous examples highlight its power. Huntley ran a multi-month loop that built “Cursed,” a complete esoteric programming language with Gen Z slang keywords—all autonomously while he was AFK. Other users have reported shipping multiple repos overnight or handling complex refactors and tests through persistent iteration. Visual contexts from discussions often include diagrams of the loop process, screenshots of Bash scripts, and examples of AI output iterations, which illustrate the self-correcting nature of the technique.

It’s important to note that this isn’t a traditional programming concept like a for or while loop in code itself, but a meta-technique for agentic AI workflows. It prioritizes persistence and self-correction over achieving perfection in a single pass, making it ideal for complex, error-prone tasks in software development.

Some Thoughts

The Ralph Wiggum Loop represents a shift toward more autonomous AI in programming, where developers can set a high-level goal and let the system iterate without constant supervision. This could democratize coding for non-experts, but it also raises questions about AI reliability— what if the loop gets stuck in a suboptimal path? Future improvements might include smarter heuristics for detecting progress or integrating with version control for better state management. Overall, it’s an exciting tool that blends humor with practicality, showing how pop culture references can inspire real innovation in tech.

What happens when the world’s most famous biohacker and a leading network state theorist team up? You get a blueprint for a “Longevity Network State.” In this recent discussion, Bryan Johnson and Balaji Srinivasan discuss moving past the FDA era into an era of high-velocity biological characterization and startup societies.

TL;DW (Too Long; Didn’t Watch)

Balaji and Bryan argue that the primary barrier to human longevity isn’t just biology—it’s the regulatory state. They propose creating a Longitudinal Network State focused on “high-fidelity characterization” (measuring everything about the body) followed by a Longevity Network State where experimental therapies can be tested in risk-tolerant jurisdictions. The goal is to make “Don’t Die” a functional reality through rapid iteration, much like software development.

Key Takeaways

Regulation is the Barrier: The current US regulatory framework allows you to kill yourself slowly with sugar and fast food but forbids you from trying experimental science to extend your life.

The “Don’t Die” Movement: Bryan Johnson’s Blueprint has transitioned from a “viral intrigue” to a global movement with credibility among world leaders.

Visual Phenotypes Matter: People don’t believe in longevity until they see it in the face, skin, or hair. Aesthetics are the “entry point” for public belief in life extension.

The Era of Wonder Drugs: We are exiting the era of minimizing side effects and re-entering the era of “large effect size” drugs (like GLP-1s/Ozempic) that have undeniable visual results.

Characterization First: Before trying “wild” therapies, we need better data. A “Longitudinal Network State” would track thousands of biomarkers (Integram) for a cohort of people to establish a baseline.

Gene and Cell Therapy: The most promising treatments for significant life extension include gene therapy (e.g., Follistatin, Klotho), cell therapy, and Yamanaka factors for cellular reprogramming.

Detailed Summary

1. The FDA vs. High-Velocity Science

Balaji argues that we are currently “too damn slow.” He contrasts the 1920s—where Banting and Best went from a hypothesis about insulin to mass production and a Nobel Prize in just two years—with today’s decades-long drug approval process. The “Don’t Die Network State” is proposed as a jurisdiction where “willing buyers and willing sellers” can experiment with safety-tested but “efficacious-unproven” therapies.

2. The Power of “Seeing is Believing”

Bryan admits that when he started, he focused on internal biomarkers, but the public only cared when his skin and hair started looking younger. They discuss how visual “wins”—like reversing gray hair or increasing muscle mass via gene therapy—are necessary to trigger a “fever pitch” of interest similar to the current boom in Artificial General Intelligence (AGI).

3. The Roadmap: Longitudinal to Longevity

The duo landed on a two-step strategy:

The Longitudinal Network State: A cohort of “prosumers” (perhaps living at Balaji’s Network School) who undergo $100k/year worth of high-fidelity measurements—blood, saliva, stool, proteomics, and even wearable brain imaging (Kernel).

The Longevity Network State: Once a baseline is established, these participants can trial high-effect therapies in friendly jurisdictions, using their data to catch off-target effects immediately.

4. Technological Resurrection and Karma

Balaji introduces the “Dharmic” concept of genomic resurrection. By sequencing your genome and storing it on a blockchain, a community could “reincarnate” you in the future via chromosome synthesis once the technology matures—a digital form of “good karma” for those who risk their lives for science today.

Thoughts: Software Speed for Human Biology

The most provocative part of this conversation is the reframing of biology as a computational problem. Companies like NewLimit are already treating transcription factors as a search space for optimization. If we can move the “trial and error” of medicine from 10-year clinical trials to 2-year iterative loops in specialized economic zones, the 21st century might be remembered not for the internet, but for the end of mandatory death.

However, the challenge remains: Risk Tolerance. As Balaji points out, society accepts a computer crash, but not a human “crash.” For the Longevity Network State to succeed, it needs “test pilots”—individuals willing to treat their own bodies as experimental hardware for the benefit of the species.

What do you think? Would you join a startup society dedicated to “Don’t Die”?

In this deep-dive conversation, Dr. Andrew Huberman joins Chris Williamson to discuss the latest protocols for optimizing the human brain and body. Moving beyond simple tips, Huberman explains the mechanisms behind stress, sleep, focus, and the role of spirituality in mental health. If you feel like your brain has been “hijacked” by the digital age, this is your manual for taking it back.

TL;DW (Too Long; Didn’t Watch)

Cortisol is not the enemy: You need a massive spike in the first hour of waking to set your circadian clock and prevent afternoon anxiety.

Digital focus is dying: To reclaim deep work, you must eliminate “sensory layering”—the buildup of digital inputs before you even start a task.

Sleep is physical: Moving your eyes in specific patterns and using “mind walks” can physically trigger the brain’s “off” switch for body awareness (proprioception).

Spirituality as a “Top-Down” Protocol: Relinquishing control to a higher power acts as a powerful neurological bypass for breaking bad habits and chronic stress.

Key Takeaways for 2026

1. The “Morning Spike” Protocol

Most people try to suppress cortisol, but Huberman argues that early morning cortisol is the “first domino” for health. By viewing bright light (sunlight or 10,000 lux artificial light) within the first 60 minutes of waking, you amplify your morning cortisol spike by up to 50%. This creates a “negative feedback loop” that naturally lowers cortisol in the evening, ensuring better sleep and reduced anxiety.

2. Eliminating Sensory Layering

Thoughts are not spontaneous; they are “layered” sensory memories. If you check your phone before working, your brain is still processing those infinite digital inputs while you try to focus. Huberman recommends “boring breaks” and a “no-phone zone” for at least 15 minutes before deep work to clear the mental slate.

3. The Glymphatic “Wash”

Brain fog is often a literal buildup of metabolic waste (ammonia, CO2) in the cerebral spinal fluid. To optimize clearance, Huberman suggests sleeping on your side with the head slightly elevated. This aids the glymphatic system in “washing” the brain during deep sleep, which is why we look “puffy” or “glassy-eyed” after a poor night’s rest.

4. The Next Supplement Wave

While Vitamin D and Creatine are now mainstream, Huberman predicts Magnesium (specifically Threonate and Bisglycinate) will be the next frontier. Beyond sleep, Magnesium is critical for protecting against hearing loss and the cognitive decline associated with sensory deprivation.

Detailed Summary

Understanding Stress & Burnout

Huberman identifies two types of burnout: the “wired but tired” state (inverted cortisol) and the “square wave” state (constantly high stress). The solution isn’t just “less stress,” but better-timed stress. Pushing your body into a high-cortisol state early in the day through light, hydration, and movement prevents the HPA axis from staying “primed” for stress later in the day.

The Architecture of Habits

Breaking a bad habit requires top-down control from the prefrontal cortex to suppress the “lower” hypothalamic urges (the “seven deadly sins”). Interestingly, Huberman notes that for many, this top-down control is exhausted by daily life. This is where faith and prayer come in; by “handing over” control to a higher power, individuals often find a neurological bypass that makes behavioral change significantly easier.

Hacking Your Mitochondrial DNA

The conversation touches on the cutting edge of “three-parent IVF” and the role of mitochondrial DNA (inherited solely from the mother). Huberman explains how red and near-infrared light can “charge” the mitochondria by interacting with the water surrounding these cellular power plants, effectively boosting cellular energy and longevity.

Thoughts and Analysis

What makes this 2026 update unique is Huberman’s transition from purely “bio-mechanical” advice to a more holistic view of the human experience. His admission of a serious daily prayer practice marks a shift in the “optimizing” community—moving away from the idea that we can (or should) control every variable through willpower alone.

The “Competitive Advantage of Resilience” is perhaps the most salient point of the discussion. In a world where “widespread fragility” is becoming the norm due to digital distraction, those who can master sensory restriction and circadian timing will have an almost unfair advantage in their professional and personal lives.