OpenAI’s audited 2025 financials leaked this week, and they are the clearest picture yet of what it actually costs to run the company behind ChatGPT. Independent journalist Ed Zitron first published the documents, and the Financial Times independently confirmed them. The headline: OpenAI spent $34 billion last year, booked $13.07 billion in revenue, and reported a net loss attributable to the company of $38.5 billion. The disclosure lands just days after OpenAI confidentially filed for an IPO that could value it north of $1 trillion.

TLDR

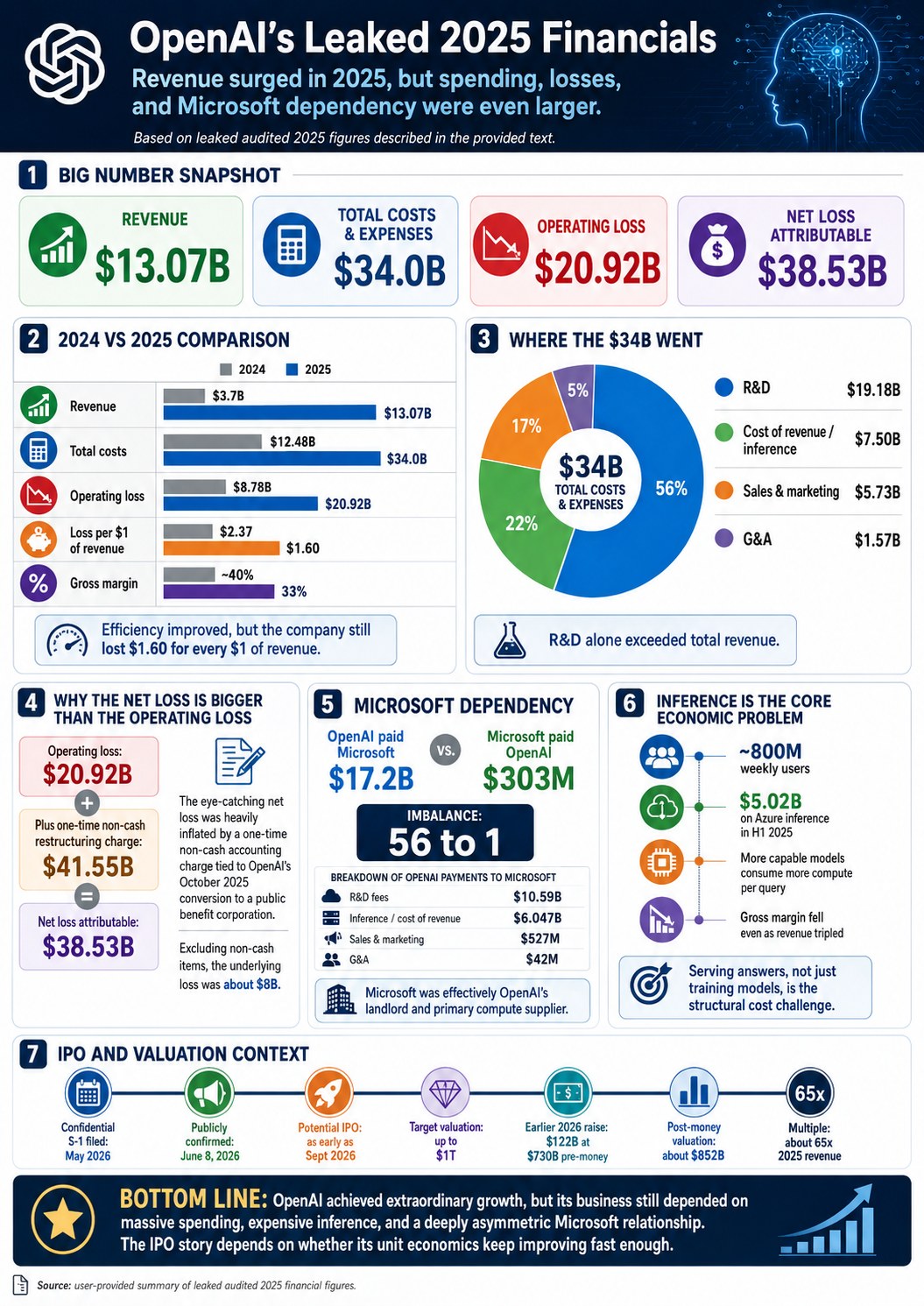

OpenAI’s audited 2025 numbers, leaked by Ed Zitron and confirmed by the Financial Times, show revenue tripling to $13.07 billion while total costs reached $34 billion, producing a $20.92 billion operating loss and a $38.53 billion net loss attributable to the company. The much larger net loss is inflated by a one-time $41.55 billion non-cash charge tied to OpenAI’s October 2025 conversion from a nonprofit to a public benefit corporation; strip the non-cash items and the loss is closer to $8 billion. R&D alone was $19.18 billion, cost of revenue (inference) was $7.5 billion, and sales and marketing ballooned to $5.73 billion. OpenAI paid Microsoft $17.2 billion in 2025 while Microsoft paid OpenAI only $303 million, exposing a deep Azure dependency. The company burned $1.60 for every dollar of revenue, down from $2.37 in 2024, and gross margin slipped from roughly 40% to 33% as more capable models consumed more compute per query. The leak arrives as OpenAI files a confidential S-1, targets a listing as early as September 2026 at up to a $1 trillion valuation, and races rival Anthropic, which is more valuable on paper and claims it is already turning an operating profit.

Thoughts

The most important thing to understand about these numbers is that there are two loss figures and the press will conflate them. The $38.53 billion net loss is the scary headline, but $41.55 billion of it is a non-cash accounting charge from converting investor convertible interests into equity during the for-profit restructuring. That charge is real on the audited statement and it will show up in the eventual S-1, but it is a one-time artifact of OpenAI’s unusual corporate history, not money that left the building. The number that describes the actual business is the $20.92 billion operating loss. That is the one to watch, and it is still enormous.

The genuinely encouraging line in the whole release is the loss-per-dollar ratio. In 2024 OpenAI spent $2.37 to generate a dollar of revenue. In 2025 that fell to $1.60. A company that is still losing $1.60 on every dollar is not a healthy business, but a company whose efficiency improved by a third in a single year while tripling its top line is at least pointed in a defensible direction. The bull case for OpenAI lives entirely in the slope of that line. If it keeps improving at that rate, the math eventually crosses over. If it stalls, the valuation is a fantasy.

The Microsoft relationship is the single most revealing disclosure, and it is wildly asymmetric. OpenAI paid Microsoft $17.2 billion in 2025. Microsoft paid OpenAI $303 million. That is a 56-to-1 ratio, and it reframes the partnership: Microsoft is not really a peer or even just an investor, it is OpenAI’s landlord and primary supplier, collecting rent on every model trained and every query answered. The April 2026 renegotiation that capped revenue-share payments at $38 billion through 2030, down from a projected $135 billion, suddenly looks less like a favor and more like OpenAI desperately trying to lower its single largest cost. The dependency cuts both ways, but right now Microsoft holds the better hand.

The structural problem hiding inside the cost of revenue line is inference. Training a model is a fixed, one-time cost. Serving it is a recurring cost that scales with every one of ChatGPT’s roughly 800 million weekly users. OpenAI spent $5.02 billion on Azure inference in the first half of 2025 alone, and the more capable its reasoning models get, the more compute each answer burns. That is why gross margin went down even as revenue went up. It is the opposite of how software is supposed to work, where the marginal cost of one more user trends toward zero. OpenAI’s marginal cost is real, large, and growing. The counterargument is that per-token inference costs have been falling roughly tenfold a year, so the unit economics could still flip. That is the entire wager.

Finally, the timing matters more than the numbers. OpenAI’s confidential S-1 means these audited figures were going to become public regardless, since the SEC requires the full prospectus at least 15 days before a roadshow. What the leak changes is who gets to study them first. Prospective IPO buyers, enterprise customers signing multi-year API contracts, and competitors now have the audited books weeks or months early, and they are reading them against Anthropic, which filed at a higher valuation and claims an operating profit. For a company asking the public markets to underwrite a $1 trillion bet on a monopoly outcome that does not yet exist, losing control of the narrative this early is not a small thing.

Key Takeaways

- OpenAI’s audited 2025 financials were first published by independent journalist Ed Zitron and independently confirmed by the Financial Times, the first verified look at the company’s books before its planned IPO.

- Revenue grew from $3.7 billion in 2024 to $13.07 billion in 2025, more than tripling year over year, making OpenAI one of the fastest-growing businesses in history.

- By the end of 2025 OpenAI was generating roughly $2 billion in monthly revenue, up from about $1 billion a quarter at the end of 2024.

- Total costs and expenses hit $34 billion in 2025, up from $12.48 billion in 2024.

- Research and development was the single largest expense at $19.18 billion, up from $7.81 billion, and exceeded total revenue on its own.

- Of that R&D spend, $10.59 billion went to Microsoft, almost certainly the GPU compute cost of training frontier models on Azure.

- Cost of revenue, the expense of serving ChatGPT responses (inference), rose from $2.65 billion to $7.5 billion.

- Sales and marketing jumped from $1.11 billion to $5.73 billion, a 418% increase.

- General and administrative costs rose from $907 million to $1.57 billion.

- The operating loss, the truest measure of day-to-day economics, grew from $8.78 billion to $20.92 billion.

- The net loss attributable to OpenAI was $38.53 billion, up nearly eightfold from $5.09 billion in 2024.

- The bulk of that jump was a one-time, non-cash $41.55 billion charge from OpenAI’s October 28, 2025 conversion to a public benefit corporation, reflecting the changing fair value of convertible interests and warrant liabilities.

- Stripping out the restructuring charge and other non-cash items such as stock-based compensation and Microsoft computing credits, the underlying loss was about $8 billion.

- Including all factors, gross net loss reached $60.35 billion, lowered to the $38.53 billion attributable figure by removing $21.82 billion attributed to noncontrolling and redeemable noncontrolling interests.

- OpenAI burned $1.60 for every $1 of revenue in 2025, an improvement from $2.37 in 2024, the clearest data point in the bull case.

- Measured as a percentage of revenue, the operating loss improved from 237% in 2024 to 160% in 2025.

- In total, OpenAI paid Microsoft $17.2 billion in 2025: $10.59 billion in R&D fees, $6.047 billion in cost of revenue, $527 million in sales and marketing, and $42 million in G&A.

- Microsoft paid OpenAI just $303 million in the same year, a 56-to-1 imbalance underscoring OpenAI’s Azure dependency.

- SoftBank paid OpenAI $867 million in 2025.

- At year-end OpenAI carried $3.64 billion in outstanding payables to Microsoft, plus tens of millions more in accrued and non-current liabilities.

- OpenAI spent $5.02 billion on Azure inference in just the first half of 2025; Azure inference from 2024 through Q3 2025 totaled $12.43 billion.

- ChatGPT serves roughly 800 million weekly users, meaning billions of queries a week, each one burning GPU time at Azure’s pricing of about $6.98 per H100 GPU-hour.

- Gross margin fell from roughly 40% in 2024 to 33% in 2025, because more capable reasoning models consume more compute per query.

- Research firm Sacra estimates OpenAI’s inference costs reached $8.4 billion in 2025 and will rise to $14.1 billion in 2026, a 68% increase.

- At year-end OpenAI held just over $50 billion in assets, with almost half in cash.

- The April 2026 Microsoft renegotiation ended exclusivity and capped revenue-share payments at $38 billion through 2030, down from a projected $135 billion, potentially saving OpenAI up to $97 billion over five years.

- OpenAI filed a confidential draft S-1 with the SEC around May 22, 2026 and confirmed it publicly on June 8, naming Goldman Sachs and Morgan Stanley as underwriters.

- The company is targeting a listing as early as September 2026 at a valuation that could exceed $1 trillion, though Sam Altman has said a public offering “may be a while.”

- OpenAI raised $122 billion earlier in 2026 at a $730 billion pre-money valuation, putting its post-money value around $852 billion.

- At an $852 billion valuation, OpenAI trades at roughly 65 times its 2025 revenue.

- Rival Anthropic also filed IPO paperwork this month after raising $65 billion at a $900-$965 billion valuation, making it more valuable on paper than OpenAI, and says it expects to report an operating profit of $559 million in the June quarter.

- HSBC analysts estimate OpenAI may need more than $207 billion in additional capital through 2030 even under optimistic projections.

- OpenAI projects profitability by 2029 or 2030; independent analysts put the more likely date at 2031 or later.

- Bridgewater partner Greg Jensen reportedly told clients the implied revenue multiples price OpenAI for “a monopoly outcome that does not yet exist.”

- Zitron separately reported OpenAI had a negative 122% non-GAAP operating margin in Q1 2026 and that ChatGPT growth has stalled, with the company projecting paid ChatGPT Plus subscriptions to fall from 44 million in 2025 toward cheaper tiers in 2026.

Detailed Summary

How the leak happened and why it matters now

The audited documents were obtained and first published by Ed Zitron on his newsletter Where’s Your Ed At, then independently verified by the Financial Times, which reviewed the same materials. That dual sourcing matters: this is not a rumor or a model, it is OpenAI’s actual audited financial statement. The timing is the story. OpenAI filed a confidential draft S-1 with the SEC around May 22, 2026 and confirmed it publicly on June 8. Under SEC rules the full prospectus must be released at least 15 days before an investor roadshow, so the 2025 numbers were going to be public soon regardless. The leak simply moved that disclosure forward, handing prospective investors, enterprise customers, and competitors an early look at the books.

Revenue tripled, costs grew faster

OpenAI’s revenue rose from $3.7 billion in 2024 to $13.07 billion in 2025, and monthly revenue reached nearly $2 billion by year-end. By almost any normal standard that is spectacular growth. The problem is that costs grew faster, reaching $34 billion against $12.48 billion the year before. The gap between what OpenAI earns and what it spends has widened every year since its founding, and 2025 is the starkest example yet. Revenue alone was outpaced by research and development as a single line item in both of the last two years.

Two loss numbers, and why both matter

There are two figures that get cited interchangeably and should not be. The operating loss of $20.92 billion is what the business spent beyond what it earned from operations: training models, serving ChatGPT, paying engineers, running marketing. The net loss attributable to OpenAI of $38.53 billion is far larger because 2025 was the year OpenAI completed its conversion from a nonprofit to a for-profit public benefit corporation, finalized on October 28, 2025. That restructuring triggered a $41.55 billion non-cash charge reflecting the changing fair value of convertible equity interests and warrant liabilities. Before the conversion, investors held convertible interest rights treated as liabilities under US accounting rules and revalued upward as OpenAI’s valuation climbed, creating the charge. It is not expected to recur. Including all minor items, gross net loss reached $60.35 billion, reduced to the $38.53 billion attributable figure after removing $21.82 billion tied to noncontrolling and redeemable noncontrolling interests, primarily the OpenAI Foundation’s stake. Strip the non-cash noise and the underlying loss was about $8 billion.

Where the $34 billion went

The spending breaks into four lines. Research and development was $19.18 billion, the largest category, with $10.59 billion of it flowing to Microsoft for training compute. Cost of revenue, the expense of serving responses to users, was $7.5 billion and captures inference, the compute consumed every time someone prompts ChatGPT or calls the API. Sales and marketing reached $5.73 billion, up 418% year over year, a striking jump for a product that grew largely by word of mouth. General and administrative costs added $1.57 billion. The shape of the spending tells you OpenAI is simultaneously racing to build better models, serve a massive and growing user base, and aggressively defend market share through marketing.

The Microsoft dependency

The most striking single disclosure is the scale of the Microsoft relationship. OpenAI paid Microsoft $17.2 billion in 2025: $10.59 billion in R&D fees for model training, $6.047 billion in cost-of-revenue for inference serving, $527 million in sales and marketing, and $42 million in G&A. Microsoft paid OpenAI just $303 million the same year. SoftBank paid OpenAI $867 million. The 56-to-1 ratio between what OpenAI pays Microsoft and what Microsoft pays back makes the structural reality plain: Microsoft is OpenAI’s largest landlord. The dynamic began shifting in April 2026, when the two renegotiated, ending Microsoft’s exclusivity and capping revenue-share payments at $38 billion through 2030, down from a projected $135 billion. That could save OpenAI up to $97 billion over five years, though Microsoft keeps its IP license through 2032 and remains the primary cloud partner.

Why inference is the core problem

Training happens once. Serving happens billions of times a day. When OpenAI releases a model it spends months and billions on training compute, a fixed cost that falls away when training ends. Inference is the opposite: every ChatGPT message runs through the model on Azure GPU hardware, consuming electricity and compute to generate a response. With roughly 800 million weekly users, that is billions of queries a week, each burning GPU time at roughly $6.98 per H100 GPU-hour on demand. OpenAI spent $5.02 billion on Azure inference in the first six months of 2025 alone. Sacra estimates full-year inference costs of $8.4 billion in 2025, rising to $14.1 billion in 2026. This is why gross margin fell from about 40% to 33% even as revenue tripled: more capable reasoning models consume far more compute per query, and revenue has not kept pace with the cost growth that capability generates.

What it means for the IPO and the race with Anthropic

OpenAI was last valued around $852 billion post-money after raising $122 billion in early 2026, which puts it at roughly 65 times 2025 revenue. It has named Goldman Sachs and Morgan Stanley as underwriters and is targeting a listing as early as September 2026 at up to a $1 trillion valuation, though Altman has hedged that it “may be a while” and that staying private might be the better course. HSBC estimates the company may need more than $207 billion in additional capital through 2030. The race is with Anthropic, which filed paperwork the same month after raising $65 billion at a $900-$965 billion valuation, making it more valuable on paper, and which says it expects a $559 million operating profit in the June quarter. The contrast is sharp: the two leading AI labs heading toward public markets at the same time, one bleeding cash at scale, the other claiming profitability, both asking investors to bet on a future that has not arrived.

Notable Quotes

“The financial condition of OpenAI is deeply concerning. $38.53 billion in losses are astronomical, and far higher than most believed it would be. Losses also appear to be mounting year-over-year at a dramatic rate, and I’m not sure how this company finds a way toward any kind of sustainability or profitability.”

Ed Zitron, the independent journalist who published the leaked audited financials

“It’s unclear what this means, nor how OpenAI reconciled the removal of $3.74 billion in costs. I will not speculate further.”

Ed Zitron, on a discrepancy he found in the restated 2024 figures

“OpenAI’s two biggest expenses are R&D and marketing. Budget cuts there, coupled with an ability to raise prices or win new sources of revenue, could see the company move into the black over time. Cutting R&D would be the most difficult part of that, given that AI companies can only hold onto their customers by generating the best-performing models.”

Jim Edwards, Fortune, on whether OpenAI has a realistic path to profitability

“What the audited documents make impossible to argue is that the path to profitability is short, clear, or cheap.”

TechTimes analysis of the leaked OpenAI financials

The implied revenue multiples price OpenAI for “a monopoly outcome that does not yet exist.”

Bridgewater partner Greg Jensen, reportedly telling clients how to read OpenAI’s valuation

“OpenAI spent $34bn last year as the ChatGPT maker poured money into a race to dominate the fast-growing AI market ahead of a planned stock market listing.”

George Hammond and Bryce Elder, Financial Times, framing the audited 2025 spend

Read Ed Zitron’s original reporting with the full breakdown here, and the Financial Times confirmation here.

Related Reading

- Ed Zitron, Where’s Your Ed At the primary source that broke the audited 2025 financials with the full line-by-line breakdown.

- OpenAI (Wikipedia) background on the company’s history, structure, and the nonprofit-to-for-profit conversion that drives the non-cash charge.

- Inference (Wikipedia) on the recurring compute cost that explains why OpenAI’s gross margin shrinks as usage grows.

- Anthropic the rival lab that filed IPO paperwork the same month at a higher valuation and claims it is already operating at a profit.

- SEC on confidential filings context for why OpenAI’s audited numbers were headed for public disclosure regardless of the leak.